Green hydrogen has become a cornerstone of the EU's industrial policy and decarbonisation plans. The EU plans to spend billions in hydrogen subsidies and provide extensive legislative support. However, its current approach risks throwing good money after bad. Producing renewable hydrogen requires a lot of energy, which means hydrogen will always remain comparatively scarce and expensive. Consequently, many hydrogen applications do not make sense at scale, neither economically nor for the climate. Yet, the EU supports all hydrogen applications without sufficiently factoring in their prospects. This policy brief argues that the EU needs to start ditching losers. Hydrogen applications that are unlikely to be viable should not get public money. To enable the EU to filter out losers, the Commission needs to take a stronger guiding role and bolster its administrative capacities.

To reach its climate objectives, the EU must radically reduce the use of fossil fuels. In some areas, such as industrial manufacturing, renewable (“green”) hydrogen has emerged as a strong contender for delivering these decarbonisation goals. Consequently, there has been much excitement in both the private and public sector, with ambitious plans for quickly scaling up the hydrogen economy in the EU. The EU is also backing those plans with substantial amounts of public funds – putting its money where its mouth is.

However, not all the buzz around hydrogen is justified. The main problem is that renewable hydrogen requires a lot of energy to produce, and will hence remain scarce and expensive. While many things are technically possible with renewable hydrogen, most of these applications simply do not make sense at scale – neither ecologically, nor economically.

EU legislation and funding schemes, however, too often do not distinguish sufficiently between those hydrogen applications that are economically viable and necessary for decarbonisation, and those that with high likelihood are a waste of time and taxpayer money. This indiscrimination is often even depicted as a virtue (for instance by Hydrogen Europe, various political parties, or industry associations). While “technology openness” is without doubt a useful concept, in the hydrogen context it is often misconstrued to justify financial support for all and any hydrogen applications, regardless of their prospects.

The EU therefore needs to recalibrate its support strategy for hydrogen:

- The EU Commission should be given more power to decide whether a hydrogen technology should receive EU support, based on technological and market developments. Being selective is not easy, but it is a necessary component of the industrial policy, which the EU has opted to pursue for hydrogen (as well as in various other areas, such as chip manufacturing).

- Industrial policy requires a strong public administration. In order to be more selective and filter out the “losers” (i.e. hydrogen applications that are highly unlikely to succeed or are too costly relative to their societal benefits), the Commission needs to further bolster its technological and economic expertise.

1. Scarce hydrogen: Only to be used for selected applications

Hydrogen can be produced using various methods. Until now, almost all hydrogen has been produced from natural gas, which creates high greenhouse gas (GHG) emissions. One approach for climate-friendly hydrogen production would be to capture and store those emissions. However, this is rather expensive and technically difficult, and not all emissions can be captured. Consequently, the EU is mainly set to pursue an approach called electrolysis, which uses electricity to split water into hydrogen and oxygen. To the extent that the electricity used is CO2-neutral, the hydrogen will be produced with zero emissions.

Doubling the hydrogen targets with REPowerEU, the EU Commission has now set a target of 20 million tonnes of renewable hydrogen being used annually within the EU by 2030. Producing these kinds of volumes requires a lot of energy: using electrolysis, their generation would take up about 30% of all electricity currently produced annually in Europe, or 90% of the EU’s solar, hydro and wind energy. Since overall demand for renewable energy is increasing, there will simply not be enough cheap renewable electricity in the EU to produce all the hydrogen needed in Europe.

For this reason, the Commission’s strategy entails importing half of the EU’s hydrogen demand from abroad. Given the higher potential for renewable energy generation in other world regions and correspondingly lower electricity costs, imports might be competitive with EU-produced hydrogen – but they will still be expensive, given the substantial costs for capital and transport (see our recent policy brief on hydrogen transport). It will also take significant time to scale up renewable hydrogen production and transportation infrastructure. In short, clean hydrogen will remain scarce and hence expensive in the EU for a long time to come.

Hydrogen applications also have relatively low overall efficiency: a significant amount of energy is lost first when hydrogen is produced (typically around 30%), and again once it is put to its final use (fuel cells in cars, for instance, lose about 40% of the hydrogen’s energy content).

Hydrogen’s scarcity and low energy efficiency have given rise to its nickname: “energy champagne”. Indeed, it will be crucial that hydrogen is used only in those areas in which no better alternative exists; otherwise, there won’t be enough hydrogen to go around, and its use would not be cost efficient.

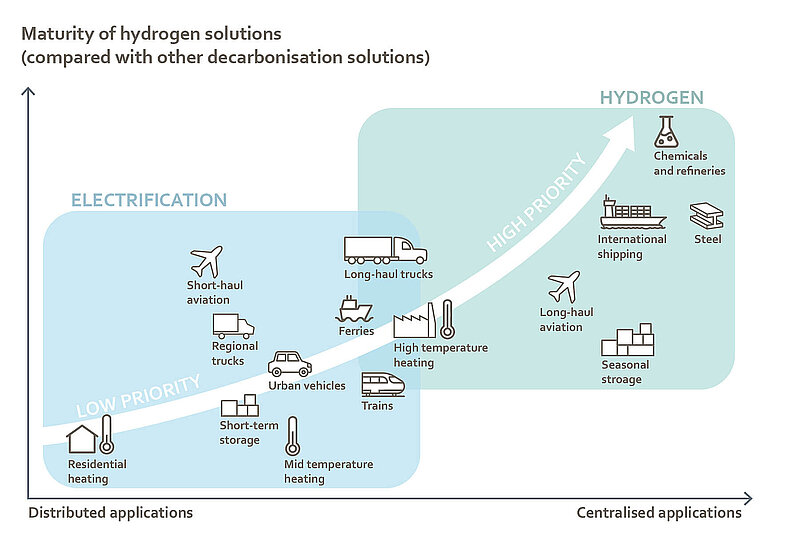

Some political and industry representatives argue against this, claiming that it is impossible to make predictions about use cases, given the uncertainty regarding future technological developments. However, in many areas, this uncertainty is bounded by the simple laws of physics. Figure 1, adopted from the International Renewable Energy Agency (IRENA), illustrates which applications should be decarbonised with hydrogen, which should not, and those which are still uncertain. So, while hydrogen could decarbonise residential heating, short-term energy storage or urban vehicles from an engineering perspective, this does not make sense from an economic or climate perspective. For long-haul trucks, ferries or high-temperature heating, some uncertainty remains as to whether hydrogen or direct electrification will be the better choice. For applications such as steel production, international shipping or chemical production, hydrogen will likely establish itself as a key technology.

Figure 1: Hydrogen application priorities according to IRENA analysis

Source: IRENA, Geopolitics of the Energy Transformation: The Hydrogen Factor

2. Technology openness: A concept with high merits, but often abused

Until a few years ago, there was little controversy in the EU about the role that governments should play in steering the economy: EU and national legislation should stick to defining “the rules” under which market actors compete with little to no government involvement. In recent years, however, the EU and national governments have been intervening more openly in the economy (EU Industrial Strategy) and have started to provide massive financial support in areas such as climate protection. Naturally, haggling over who gets the subsidies under which conditions has followed. In this context, the concept of “technology openness” is often invoked to justify broadening public support to cover additional technologies.

Technology openness can be understood as policymakers specifying an objective without defining the method or technology to reach it, as well as providing financial support without discriminating according to the technology employed by the beneficiary. Competition between different technologies and companies are then expected to deliver the objective efficiently – “may the best technology win”. The advantage of technology openness is that it avoids the need for governments and bureaucrats to “pick winners”, i.e. selecting the technology (or even the individual company) that will be best suited to achieve a certain objective. Picking winners is difficult and has a poor track record, given uncertainty about future technological developments, governments’ necessarily limited knowledge, and the risk of political capture by industry interests (Rodrik 2014).

However, “technology openness” on its own is not a sufficient justification for extending public support to cover a given technology (like a hydrogen application) for three reasons:

First, a sensible interpretation of “technology openness” does not imply that all and any technologies should receive support. The main reason for providing government support in the first place is to reach a certain objective, such as alleviating a market failure to protect the climate. Consequently, any support should advance the policy’s overarching objectives, and this means excluding technologies that for whatever reason are not compatible with the policy goal. The EU could, for instance, set up a funding scheme with the objective to “decarbonise domestic heating”, which could plausibly encompass hydrogen heating as an eligible technology. However, given the EU’s objective to bring total energy use down, it can be perfectly sensible to design funding schemes which ensure that only heating technologies passing a certain threshold of energy efficiency are eligible for public support, which would likely render hydrogen ineligible. Note that the scheme could still be “technology open” for all energy-efficient technologies, harnessing the positive effects of competition between them.

Second, providing support in a technology open manner can have prohibitively high costs. A wide interpretation of “technology openness” in providing public support entails not just equal support for the competing technologies (e.g. subsidies for different emission-neutral cars) – it also requires creating the conditions necessary to enable these technologies (e.g. subsidies for building charging or refuelling infrastructure). This is the approach the EU has taken, for instance, in the Alternative Fuels Infrastructure Regulation. However, there are typically a high number of technologies that could deliver the same objective. In the example of charging/refuelling stations for emission-neutral cars, should public money be used just for electric charging stations, or also for hydrogen refuelling stations? What about charging infrastructure for more obscure technologies, such as liquid nitrogen engines? Clearly, being fully “technology open” and supporting the build-up of infrastructure for each and every technology would have prohibitively high costs. Therefore, some criteria have to be employed in order to decide which technologies to support.

Third, in some cases, technology openness is too slow in delivering the objective. While a “technology open” approach is demonstrably good at ensuring that the technology best suited to deliver the objective succeeds eventually, it is not necessarily good at delivering the objective with highest possible speed. If speed is a priority (as with climate protection), it can be better to concentrate all efforts on a single technology, even at the risk of eschewing an alternative technology that may have been slightly better. This is especially the case where there are sizable economies of scale, or if uncertainty about which technology will be dominant holds back investment in the technology and its related ecosystem.

For these reasons, the EU must decide on a case-by-case basis if support should cover hydrogen technology or not. In addition to harnessing the positive effects of competition between some technologies and avoiding the need to “pick winners”, EU support also has to “let losers go” (Rodrik 2010), i.e. exclude hydrogen applications that are simply not promising enough. Making these decisions inevitably comes with some mistakes, but not making them would be even more costly.

3. Some EU hydrogen support disregards climate and economic constraints

The EU is highly active in pushing renewable hydrogen forward, with broad backing from the EU institutions, member state governments and the private sector. Following Russia’s invasion of Ukraine, hydrogen has been assigned an even larger role with respect to energy security and accelerating the green transition (REPowerEU).

EU support for green hydrogen takes many forms, including binding hydrogen targets, coverage under CBAM, and close cooperation with the private sector. On the financing side, the EU provides direct financial support and has also made it easier for member states to use national funds to subsidise hydrogen applications. The large volume of support is justified in order to quickly scale up the production of renewable hydrogen and incentivise decarbonisation. However, the EU’s support is not selective enough. Currently, anything and everything in the hydrogen space is eligible to receive support.

For instance, the EU funding programme Horizon Europe, which focuses on Research and Development, financially supports hydrogen projects across the whole spectrum (such as hydrogen aviation, rail, fuel cells, steel, heating, and much more). Another important funding vehicle is the Important Projects of Common European Interest framework (IPCEIs). Recently, two hydrogen IPCEIs were approved by the EU Commission, totalling €10.6 billion and spanning projects from 16 member states (many of those projects are part of the Recovery and Resilience Plans and are hence ultimately financed by the EU). The projects also span large parts of the hydrogen spectrum, including e.g. support for hydrogen cars. Three examples illustrate the issues of the current approach.

First, domestic heating with hydrogen continues to receive EU institutional support and taxpayer money. It is included in the EU hydrogen strategy (COM 2020), and consequently also supported by the Clean Hydrogen Partnership, where heating with hydrogen makes up a whole pillar in the strategic research agenda, and accordingly receives EU funding. Residential hydrogen heating is also covered by the European Clean Hydrogen Alliance, which dedicates one of its six roundtables to “residential applications”, i.e. mostly heating. One reason for the EU support is likely that gas companies and gas network companies and their lobby organisations have been pushing for it. They could continue their current business model with relatively limited changes: the appliances (such as boilers) would be similar to the ones currently used for natural gas, and hydrogen would be delivered via pipelines to houses, requiring a very extensive hydrogen distribution network (replacing or repurposing the natural gas pipes).

However, from a technological and scientific perspective, it has become clear that other technologies, such as heat pumps, are superior. A recent review of 32 independent studies on the matter (Rosenow 2022) concludes that “hydrogen use for domestic heating is less economic, less efficient, more resource intensive, and associated with larger environmental impacts”. Given the large amounts of energy needed to produce hydrogen and its scarcity in the foreseeable future, there seems to be little scope for technological innovations to change this assessment.

The main concern with residential hydrogen heating is not that the EU research funds would probably be better spent on other areas. But what must be avoided is that EU support for hydrogen heating triggers some regions to build up expensive infrastructure (hydrogen pipes to residential houses). Eventually, the higher system costs, compared to heat pumps, would have to be borne by taxpayers or reflected in households’ energy bills.

Second, blending of hydrogen, i.e. mixing small quantities of renewable hydrogen into the natural gas grid, thereby reducing the gas grid’s carbon footprint, provides another negative example. Like domestic heating, this approach is being pushed by industry interests, but does not have much merit, which is underscored by various independent evaluations (Fraunhofer 2022). The main drawback lies in the fact that scarce hydrogen would be wasted in sectors such as domestic heating, instead of being used exclusively in those sectors that cannot be directly electrified, like heavy industry. Moreover, blending would likely also increase overall costs for end-users and infrastructure operators, even at low blending levels. While the Commission even points out these disadvantages in the REPowerEU Staff Working Document, it is still part of the REPowerEU hydrogen targets, and blending projects can still receive EU funding.

A third example, with slightly different characteristics, is the mandatory build-up of hydrogen refuelling stations. Currently, the Regulation for Alternative Fuels Infrastructure is negotiated at the EU level, which will (unless changed in the ongoing trilogues) mandate frequent charging and refuelling stations along major roads, including for hydrogen, by 2030. These hydrogen stations are very expensive and will require public subsidies. They will also require an expensive hydrogen distribution network to get the hydrogen to the stations, which again will be borne at least partially by the taxpayer.

However, for road transport, hydrogen does not look like a promising solution, at least for light vehicles. The race seems to have been already decided in favour of battery-electric cars, which are much more energy efficient, much less complex to build, and much cheaper than hydrogen (fuel cell) cars. In line with these fundamental advantages (which are unlikely to change in the future), battery-electric vehicles have an enormous lead over hydrogen cars. Whereas only a few thousand hydrogen cars were sold last year, sales for battery-electric cars were already in the millions. By now, almost all manufacturers have strategically aligned their manufacturing towards battery-electric cars.

For heavy-duty vehicles, such as trucks, more uncertainty remains, and hydrogen vehicles might position themselves successfully in the market. However, it is quite possible that within the next few years, battery vehicles will emerge as the dominant technology for heavy duty transport as well. But the EU institutions do not seem to cater to this possibility; if, for instance, battery improvements were to occur in the coming years that render hydrogen road transport uncompetitive, there is no straightforward way for the binding 2030 targets on hydrogen refuelling infrastructure to be removed quickly. This would mean that even if the chance of success for heavy-duty hydrogen vehicles becomes miniscule, the refuelling stations would still have to be built, wasting taxpayer money.

4. How the EU can more actively steer the development of the hydrogen economy

The above cases are emblematic of a systemic issue that pervades the current support strategy for hydrogen: EU legislation and funding are not sufficiently selective in their support. Being more selective and “letting losers go” would allow for the hydrogen policy to be better aligned with climate and energy objectives and necessitate less public financial support. This requires the EU to take up the challenges of industrial policy and make tough choices. To enable the EU to make these choices, two aspects are especially important.

A stronger guiding role for the EU Commission:

The “power to decide” is not easy to wield, since mistakes are possible. But not exercising it would clearly be worse, and waste substantial resources as well as time to reach climate neutrality. Since the decisions as to whether a hydrogen technology should receive EU support must be based on technological and market developments, the EU Commission is the right body in the EU to take these on.

To be able to “let losers go”, it should be mandatory to regularly check whether applications still hold potential. In the case of the refuelling stations, for instance, this could involve empowering the Commission to reassess the mandatory targets in the Regulation on a regular basis, allowing them to be altered or removed. If it were to become evident within a few years that heavy-duty hydrogen trucks will not succeed, there is no point in continuing to build hydrogen refuelling stations until 2030. This reasoning of course extends to related areas, such as mandating hydrogen airport infrastructure, for which similar precautions should be taken.

Other hydrogen applications with very low chances of success, such as blending or domestic heating, do not have mandatory targets in EU law. But the Commission should still take a stronger guiding role on these issues, reflecting that better alternatives exist. This includes taking an explicitly dismissive stance towards these hydrogen applications in documents like the Hydrogen Strategy or REPowerEU, and ruling them out for support. Clearly dismissing certain applications would also help to reduce lingering uncertainty that has been inhibiting alternative technologies, such as heat pumps.

Strengthening public administration:

To distinguish applications that are worthwhile from those that most likely are not, a deep understanding of hydrogen technologies and the underlying business cases is necessary. The EU Commission in particular needs to possess hydrogen and energy expertise, with a sufficient number of staff. For one, this is needed as the analytical counterweight to output by lobbying groups, which are heavily active in the hydrogen space, and which are tightly interwoven with the Commission through various advisory bodies. There are more energy lobbyists in Brussels than there are employees in DG ENER. Of course, lobby groups need to be heard, and much of the transformation will be delivered by the current market incumbents, whose insights are crucial in guiding the green transition. But in the hydrogen space, there seems to be a particularly high risk that policies could become sub-optimally tilted towards the interest of incumbent industries, which try to continue their business models with as little change as possible. This is evident for instance in the loud voice of gas network operators, which manage to keep hydrogen heating and blending proposals in the policy discussion.

To keep the administration lean, expertise can also be hired externally for certain tasks, for instance for scientific or technological analyses. However, some caution is needed here to ensure that the hired expertise is truly objective. For instance, a study on hydrogen costs and benefits commissioned by the EU Commission was conducted by the same consultancy that supports the gas network operators in their influential plans for a hydrogen pipeline network. While this is not necessarily a problem (various EU safeguards already exist to avoid conflicts of interest), it is important that the relevant DGs in the Commission (in particular DG ENER and JRC) possess sufficient expertise to competently navigate this close cooperation with the private sector.

Bolstering the Commission’s capacities and staff would also be beneficial for the approval of state aid. In the case of the hydrogen IPCEIs, the approval by DG COMP – despite being prioritised and accelerated – still took quite long, and put the timeline of hydrogen projects in jeopardy (including those with milestones in the Recovery and Resilience Plans). This is part of the reason why the German and French governments are calling for cutting the IPCEI approval times by half. If increasing the number of permanent staff is not feasible or considered too costly, alternatives should be explored, such as seconding more national experts from national ministries to DG COMP, or hiring external staff during peak approval times.

5. Conclusion

The existence of uncertainty does not justify EU support for every application in the hydrogen space regardless of its probability of success. The expected return of financial support needs to be positive: a Euro spent on hydrogen support should in expectation deliver societal value equivalent to at least one Euro. EU legislation and financial support need to better reflect this simple idea, and the EU Commission needs to boost its capacities to make judgements on the viability of hydrogen applications. Those applications that are not viable must be ditched.

This is not only relevant for hydrogen, but applies analogously to other industrial policy support provided by the EU. Given that stronger industrial policy will most likely be part of the EU reaction to the US Inflation Reduction Act, EU regulatory and financial support is set to increase across the board, raising the stakes – and cost – of inefficient policy decisions.